Job creation is a pivotal aspect of economic growth and stability, and one of the robust tools for fostering this growth in the United States is the SBA 504 Loan Program. Job Creation and SBA 504 Loans are intrinsically linked, as the program is designed to provide financing for the purchase of real estate, machinery, and other fixed assets, thereby stimulating job creation and retention. Offered by the U.S. Small Business Administration (SBA), the 504 loans are facilitated through Certified Development Companies (CDCs), SBA-approved nonprofit organizations that serve their local communities by promoting economic development.

A significant objective of the SBA 504 Loan Program is to stimulate job creation and retention. Businesses applying for a 504 loan often need to meet certain job creation or community development criteria, underscoring the program’s broader economic goals. This long-term financing tool is especially attractive due to its low down payment requirements and fixed interest rates, easing the path of business owners toward expansion and sustainability. Understanding the terms, benefits, and eligibility requirements of the SBA 504 Loan Program is crucial for any business considering this financing option.

Key Takeaways

- The SBA 504 Loan Program is aimed at economic development through business expansion and job creation.

- These loans offer long-term financing with fixed interest rates for major fixed assets.

- Eligibility for SBA 504 loans includes meeting job creation criteria or community development goals.

Understanding the SBA 504 Loan Program

The SBA 504 Loan Program, administered by the Small Business Administration, provides a reliable source of financing for small businesses looking to acquire or improve real estate, machinery, or equipment. This program works in conjunction with Certified Development Companies (CDCs) to promote economic growth.

Basics of the 504 Loan Program

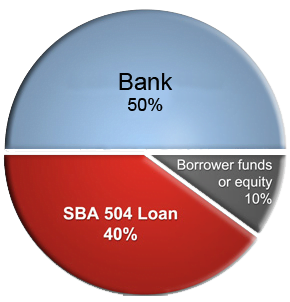

The 504 Loan Program is a powerful tool for small business growth, offering long-term, fixed-rate financing. It is designed to foster economic development by financing fixed assets that promote business expansion and job creation. Under this program, projects are typically funded by:

- 50% from a private-sector lender

- 40% from a CDC, guaranteed by the SBA

- 10% equity from the small business borrower

These loans are capped at $5 million for most businesses, but certain energy projects may qualify for more. Borrowers benefit from the low down payment and fixed interest rates which are below-market, mitigating the risk for both the lender and the borrower.

Eligibility Requirements for Borrowers

To qualify for a 504 loan, businesses must:

- Operate as for-profit entities within the United States

- Have a tangible net worth of less than $20 million

- Have an average net income of less than $6.5 million after taxes for the preceding two years

Additionally, the project being financed must be for assets that benefit the business and fall into one of the following categories:

- The acquisition or improvement of land, buildings, or infrastructure

- The purchase of long-term machinery or equipment

Certified Development Companies (CDCs) have a pivotal role in the 504 Loan Program. Most are nonprofit corporations that are regulated by the SBA to work with borrowers and lenders. Their goal is to support economic development within their communities by partnering with conventional lenders to provide the 504 Loan Program’s financing structure.

The Application Process and Terms

When seeking an SBA 504 loan, applicants must navigate a structured process and familiarize themselves with specific loan terms and repayment conditions. These are pivotal to securing the needed funds for significant business investments in assets such as real estate or equipment.

Steps to Apply for a SBA 504 Loan

Applicants initiate the process by first identifying a Certified Development Company (CDC). A CDC collaborates with lenders to furnish 504 loans and is mandated to promote economic growth within its community. The typical application steps are as follows:

- Eligibility Check: Verify that the business meets the requirements, including an average net income of less than $6.5 million after federal income taxes for the two years preceding the application and a tangible net worth of less than $20 million.

- Prepare Documentation: Assemble the necessary paperwork, including tax returns, financial statements, and a business plan that demonstrates job creation potential.

- Credit Score Review: Ensure that personal and business credit scores are in good standing, as they will impact the approval process.

- Application Submission: Working with a CDC, submit the full loan application including a proposed plan for how the loan will contribute to job creation or community development.

- Loan Approval: If the application is successful, the applicant will proceed with closing and disbursing of the loan.

Understanding Loan Terms and Repayments

The terms and repayments of an SBA 504 loan are crucial for borrowers to comprehend:

- Loan Amounts: SBA 504 loans can finance up to $5.5 million for certain energy projects, and $5 million for other projects.

- Down Payment: Borrowers typically contribute a down payment of at least 10%, which may increase depending on the business’s financial situation and the project type.

- Interest Rates: The interest rates are fixed for the life of the loan, usually below market rates, offering affordability and predictability.

- Repayment Terms: These loans come with terms of 10, 20, or 25 years, dedicated to long-term investments, with the repayment structure designed to maintain cash flow for the business during the term of the loan.

How Job Creation and SBA 504 Loans Drive Economic Development

The SBA 504 Loan is a powerful tool for small businesses aiming to enhance their operations and stimulate economic growth. Strategically using this loan can unlock the potential in acquiring substantial assets and developing commercial spaces.

Purchasing Major Fixed Assets

A core application of the SBA 504 loan is purchasing major fixed assets that spur business development and job creation. Fixed assets include heavy machinery and equipment that are essential for a company’s operations but require significant capital investment. Businesses can take advantage of the SBA 504 loan to maintain competitive leverage by ensuring their facilities are equipped with state-of-the-art technology. Such investments typically offer long-term productivity gains and are a crucial step in a small business’s growth trajectory.

Real Estate and Construction Financing

For companies looking to expand their physical footprint, the SBA 504 loan provides an avenue for financing the purchase or improvement of real estate and land. This includes the construction of new facilities or modernization of existing ones. The terms of the financing are designed to be favorable for small businesses, managed through a Certified Development Company, or CDC, focusing specifically on promoting economic development. Utilizing this loan for real estate development or construction projects not only facilitates a more robust operational capacity but also contributes to local community growth, aligning with the aims of economic development.

Frequently Asked Questions

The SBA 504 Loan Program is a powerful tool for enhancing economic development and fostering job creation. Through these FAQs, one can gain clarity on eligibility, compare loan rates, understand different SBA loan programs, and discern the specifics of job creation requirements and payment calculations.

What are the eligibility criteria for obtaining an SBA 504 loan?

To be eligible for an SBA 504 loan, applicants must operate as a for-profit business, have a tangible net worth of less than $20 million, and have an average net income of $6.5 million or less after federal income taxes for the two years preceding the application. The project financed must also be used for eligible purposes like buying land or improving facilities.

How do SBA 504 loan rates compare to traditional commercial loans?

SBA 504 loan rates are typically lower than traditional commercial loan rates because they are backed by the federal government. Additionally, they offer long-term, fixed-rate financing that can provide small businesses with predictable payments and the opportunity to manage their cash flow more effectively.

What are the differences between SBA 504 and 7(a) loan programs?

The primary difference is that SBA 504 loans are specifically for real estate and major equipment, aiming to promote economic development. On the other hand, SBA 7(a) loans are more general purpose, covering a wider range of business needs such as working capital. Each has different maximum loan amounts and terms, affecting their suitability depending on the borrower’s needs.

How can entrepreneurs use the SBA 504 loan to finance their startups?

Entrepreneurs may use SBA 504 loans to finance the purchase of existing buildings, land, and long-term machinery, as well as the construction or conversion of facilities. Startups might find these loans especially advantageous for significant upfront capital investments that are typically required to get businesses off the ground.

What are the job creation requirements associated with SBA 504 loans?

The job creation requirements for SBA 504 loans stipulate that for every $90,000 or $100,000 loaned—depending on the industry—one job must be created or retained within two years. This requirement aims to ensure that the benefits of the loan extend beyond the business itself and into the wider community.